A recent policy paper, developed under the Switch to Circular Economy Value Chains project, evaluates how EU policy is driving the transition to the circular economy, its impact on global value chains and how developing country producers can navigate changing markets.

The policy paper will detail on

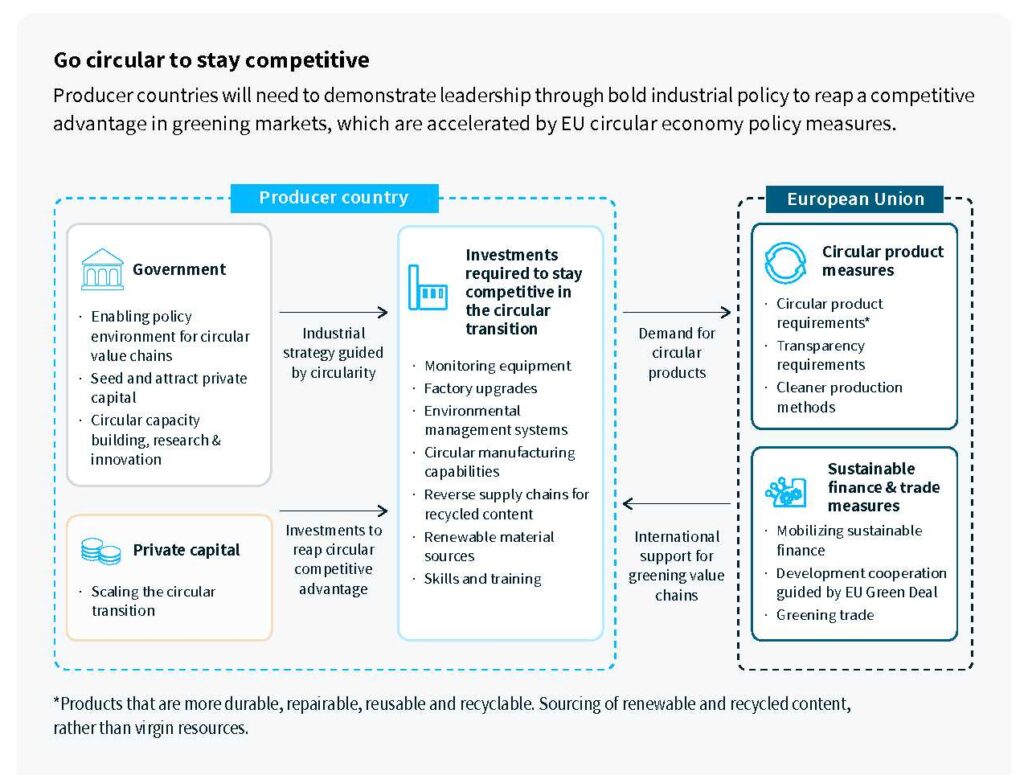

- EU policies drive the greening of global value chains

- The plastics and plastic packaging value chain

- The Textile and garments value chain

- International support for the circular transition in developing countries

The current plastics and textiles value chains are extractive and linear, resulting in large quantities of resource use, greenhouse gas emissions, pollutants, and waste. The EU Circular Economy Action Plan (CEAP 2.0) aims to shift these value chains towards circular models by targeting sourcing, design, manufacturing, distribution, sale and waste management. CEAP 2.0 policies, such as those for circular plastics, will increase in ambition and result in higher costs for producers, greater emphasis on product circularity, and more restricted plastic waste trade.

Producers in developing countries are facing increasing pressure to provide recyclable packaging for products to access the EU market and multinationals’ portfolios. Sourcing high-quality recycled content will be a critical strategy to ensure resilience, and producers who shift to circular packaging solutions can expect stronger demand, especially if materials are traceable and impacts are third-party verified.

The textiles and garments value chain also faces legislation for circularity, with the EU’s new sustainable textiles strategy being a key development. These changes are expected to take effect as soon as 2025 and may present short-term challenges for producer countries. However, adopting relevant circular practices can help manage environmental impacts and stay competitive in greening global markets. The EU will continue to support its trading partners in developing circular plastics and textiles industries worldwide.